In our fifth and final installment of our TSO series, we take a deep dive into four policy, regulatory, and process recommendations that will help further unlock the value of storage as a transmission solution, helping us modernize the grid to version 2.0.

If you’re new to the series, read our overview of each of the challenges and catch up on the first four: intermittency and congestion, weakening grid stability, reduced visibility of grid assets and new asset investment amidst decreased capital availability.

Grid 2.0: Building the Backbone of the Energy Transition

The complex processes of grid planning and operation have historically been geared toward large, centralized generators and one-way power flow from generation to load. This process doesn’t match today's reality of renewable-dominated power grids.

As regulators try to accelerate the transition from thermal-based generation to renewables, they must emphasize expanding, securing, and modernizing transmission systems. Doing this requires new, innovative grid technologies.

As a transmission solution, battery-based energy storage is capable of providing congestion relief and contingency management, enhancing the utilization of existing and new transmission systems alike. Despite these capabilities, many system operators are still subject to outmoded planning and regulatory frameworks that prevent storage from being proposed or selected as a transmission solution.

Designing Policy for a Renewable Grid

The development of storage-as-transmission-assets (SATA) within the power grid is directly dependent on the existence of a suitable policy and regulatory framework. Grid operators simply can’t go around the existing regulatory processes and laws that govern them to deploy energy storage as a transmission asset, regardless of the value they may see in it.

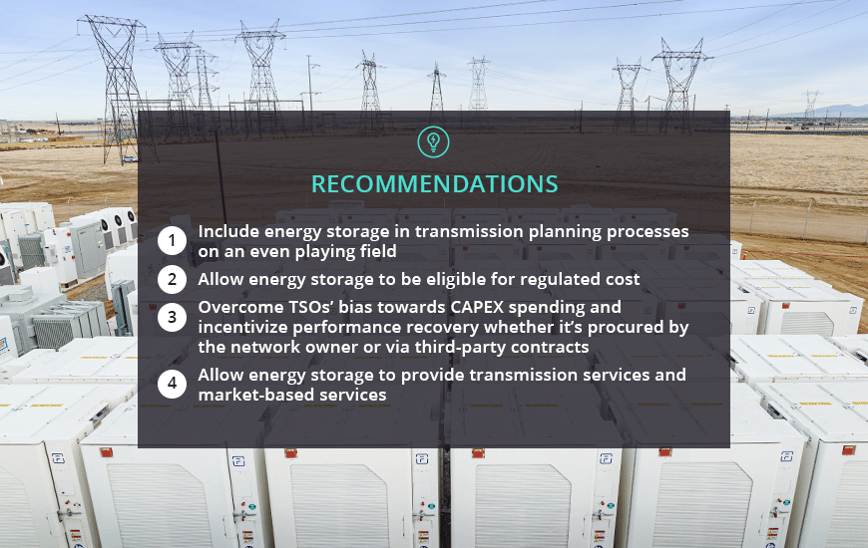

To help further unlock the value of storage, we have outlined four policy, regulatory, and process recommendations.

#1

Include energy storage in transmission planning

processes on an even playing field

How It Would Work

To maintain a reliable and least-cost system, in transmission planning, TSOs identify required transmission solutions by simulating power flows based on future load and generation assumptions. Today, most regulations only allow TSOs to include traditional grid infrastructure (e.g. poles and wires) as eligible solutions, despite energy storage’s ability to optimize transmission infrastructure.

Grid planning should include provisions to allow the identification and selection of storage and other innovative technologies in grid development plans, transparently and fairly. Cost-benefit analyses need to compare different technology options and evaluate social and ecological elements of grid design as well as economic ones.

Where It Has Worked

2019 EU legislation on electricity market rules required TSOs to “fully take into account the potential for the use of demand response, energy storage facilities or other resources as alternatives to system expansion". This is an important beginning, but the directive lacks the teeth to force TSOs to consider energy storage on par with traditional grid infrastructure. Three years on, the legislation has yet to spur a substantial uptick of SATA solutions in Europe or even in TSOs’ planning processes. This said, initial results of the legislative change are visible, as two German TSOs are currently procuring 450 MW SATA solutions.

Out of the U.S.’s seven regional transmission operators/independent system operators (RTOs/ISOs), California ISO and Midcontinent ISO (MISO) have regulator-approved tariff language around energy storage as a transmission asset. The language states that energy storage can legally provide transmission services and must be evaluated on an even playing field with traditional grid infrastructure.

#2

Allow energy storage to be eligible for regulated cost recovery

whether it’s procured by the network

owner or via third-party contracts

How It Would Work

Traditional transmission infrastructure is paid via a regulated cost recovery: transmission owners get guaranteed and fixed returns to build (and in some markets, maintain) grid infrastructure. SATA has demonstrated its ability to provide valuable transmission services, yet regulations keep TSOs from earning returns on their SATA investments. When fulfilling a transmission service, SATA should be eligible for the same treatment as any other piece of transmission infrastructure (e.g., substation equipment, poles, and wires).

Where It Has Worked

The same piece of EU legislation that required TSOs to consider energy storage in their planning processes also enabled EU member states to “allow transmission system operators to own, develop, manage or operate energy storage facilities, where they are fully integrated network components and the regulatory authority has granted its approval.” This clears the way for TSOs to buy storage or contract services from storage assets and incorporate them into their cost base accordingly.

MISO’s Federal Energy Regulatory Commission (FERC)-approved Storage as Transmission Only Asset (SATOA – a version of SATA that excludes dual-use applications) allows energy storage to demonstrate that it is providing regulated transmission services and thus earn regulated cost recovery if it is selected in the MISO Transmission Expansion Plan (MTEP). In this situation, energy storage is essentially on equal footing with any other transmission solution.

#3

Overcome TSOs’ bias towards

CAPEX spending and incentivize performance

How It Would Work

Most TSOs are incentivized to build assets (CAPEX) instead of procuring services (OPEX). Under this incentive structure, TSOs have a harder time justifying the lower-cost purchase of an energy storage system or procurement of energy storage services when they could instead spend more on a traditional transmission line and generate larger regulated returns.

Newer approaches focus on TSOs delivering better service to customers, operating safely, and lowering their emissions, irrespective of whether they use CAPEX, OPEX, or a mix to do so. This helps level the playing field for innovative technologies like energy storage systems.

Where It Has Worked

Beginning in 2013, the United Kingdom’s Office of Gas and Electricity Markets rolled out a new framework for utility compensation. Called RIIO (Revenue = Incentives + Innovation + Outputs), the framework moves away from the traditional cost-of-service model and instead rewards utilities for:

- Minimizing interruptions

- Lowering emissions

- Reducing grid connection time

- Satisfying customers

- Aiding vulnerable customers

- Operating safely

- Performance against these targets impacts the financial rewards and penalties utilities face, ultimately affecting their annual rate of return.

Additionally, RIIO combines a portion of utilities’ CAPEX and OPEX into one asset class called total expenditures (TOTEX), for which utilities receive a single rate of return. This eliminates the CAPEX bias, incentivizing utilities to instead pursue the most effective solution.

#4

Allow energy storage to provide transmission services

and market-based services

How It Would Work

When storage assets provide transmission services such as congestion relief, they are only deployed in those applications during times of congestion.

Idle storage assets could be deployed into wholesale market applications, earning additional revenue for performing other vital grid services like shifting energy from low to high price periods. However, given TSOs are regulated entities that own assets with different risk profiles and operate with lower profit caps than non-regulated entities, they are kept from competing in wholesale markets.

Dual-use storage assets – assets earning revenue in the competitive market and through regulated services – could be commercially divided. Regulated services could be provided under the direction and control of the TSO, and market-based services provided under the direction and control of independent power companies.

By unlocking the full value of energy storage assets to provide any and all services the physical infrastructure is capable of, end consumers will reap the rewards of a more efficient, secure, decarbonized, and low-cost power system.

Where It Has Worked

In 2017, FERC published a policy statement supporting the concept of energy storage assets being compensated for dual use in the U.S. Acting on that notion, MISO began a stakeholder process in 2020 to expand its SATOA tariff to “be used to provide market services when available."

This would be the first such ruling in the U.S. and a significant breakthrough for power markets across North America. After a pause to finalize their SATOA rules, MISO has reengaged the topic and is actively working with stakeholders to design a system that could be brought before FERC for consideration.

In Australia, the Victorian Big Battery operates as a dual use asset. In the summer, a 250 MW/125 MWh portion of the 300 MW/300 MWh asset is contracted to a control scheme that increases the capability of the Victoria to New South Wales Interconnector to urgently upgrade the transmission network during the hottest months. The other 50 MW/175 MWh of the Big Battery participates in energy and ancillary service markets. For the rest of the year, the whole asset participates in these markets.

What Lies Ahead

The need for global grid modernization is clear. Over this five-part series, we’ve demonstrated how this need presents TSOs with significant challenges, but also with meaningful opportunities.

Multi-decade network planning, upgrades, and deployment will not allow TSOs to keep pace with either the supply shifts driven by far-reaching global forces or the most dramatic demand variance since industrialization. System operators must instead collaborate with regulators and technology providers to chart a path forward. One that allows battery storage and other emerging technologies to participate in transmission services.

In so doing, they will reduce unnecessary costs to the system and better position the public to capture the potentially large and diverse benefits of increased battery adoption. The end result: reliable, renewable, affordable power.

Curious about other T&D topics?

Check out our other posts on how energy storage can help overcome transmission system challenges:

TSO Series: Five Challenges TSOs will Face Today and in the Future

TSO Series | Challenge 1: Intermittency and Congestion

TSO Series | Challenge 2: Weakening Grid Stability

TSO Series | Challenge 3: Reduced Visibility of Grid Assets

TSO Series | Challenge 4: New Asset Investment Amidst Decreased Capital Availability